Break free from the chains of debt, including that stubborn mortgage, within a mere 3-5 years.

JOIN NOWDear Debt-Burdened Friend,

Let's talk hard truths. The majority of people are shackled by debt, be it credit cards, loans, or even the mighty mortgage. But guess what? The chains of debt don't have to hold you captive for decades. In fact, within a mere 3-5 years, you could break free, including that mortgage! (Without having to sacrifice your lifestyle or pinch your pennies.)

"But hold on," you might say, "that's only possible if you're raking in big bucks or living on beans and rice, right?"

Not so fast. The magic lies in a system that even individuals with modest incomes can leverage. Prepare to obliterate your debt in record time without living like a hermit or cutting out all the fun.

The Secret Revealed

Your income isn't just a paycheck; it's a potent tool for constructing wealth. The hitch? Most folks let their income slip through their fingers like sand. They invest in liabilities and compound their troubles with debt, locking themselves into a never-ending cycle. Years roll by, interest piles up, and their debt mountain stays put.

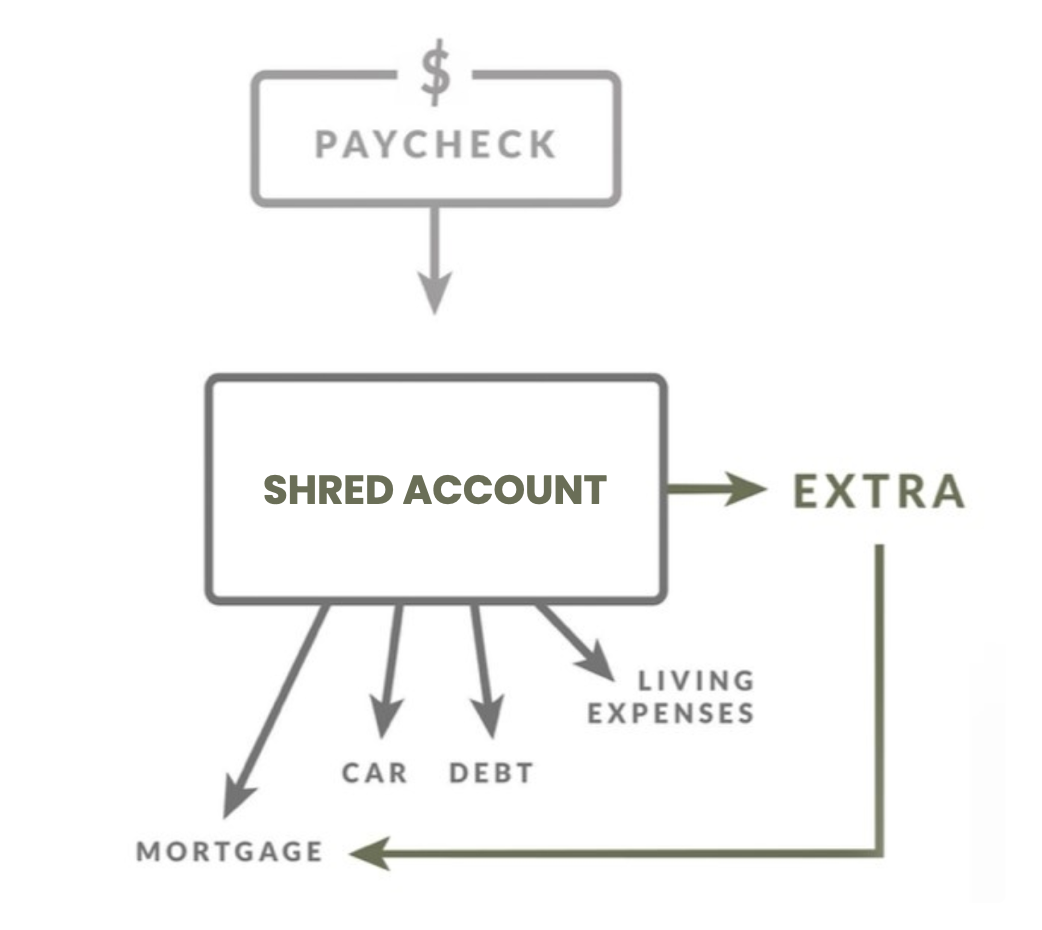

Your income should be flexing its muscles in these four ways:

- Cover Expenses

- Crush Debt

- Build Wealth

- Fuel Fun and Goodness

Sound simple? Well, it's easier said than done. Many ace the first and last steps but falter in the middle, which are the bedrock of financial freedom.

The Paradox of "Expert" Advice

You've been obediently following the gurus' advice, right? Multiple savings accounts, obsessing over emergency funds, modestly drip-feeding investments, and throwing an extra Benjamin at your mortgage monthly, hoping to shorten its leash.

Solid moves, sure. But here's the kicker: There's a faster, more effective way.

THE PROBLEM WITH CONVENTIONAL WISDOM? YOU MIGHT END UP IN AVERAGEVILLE, TRAPPED LIKE MOST, STRAINING FOR RETIREMENT, ENDLESSLY FRETTING ABOUT THE MARKET'S TWISTS AND TURNS.

You'll have those emergency funds and savings, but guess what you'll also have spent? Countless benjamins in needless interest payments. Those same benjamins could supercharge your wealth journey, ignite real prosperity, and build generational wealth.

Introducing the Game Changer:

The Shred Method™

Get ready for a financial game-changer, one that'll have your banker scratching their head. It's a debt-crushing machine, tearing through your financial burdens like a wrecking ball. Say goodbye to your mortgage and watch your debts disappear as your wealth skyrockets. No more nickel-and-dime strategies – The Shred Method™ is here to kick your debt to the curb, like yesterday's old news.

Unlocking the Door to Prosperity

As you master this technique, watch these marvels unfold:

- Increased Disposable Income: Monthly breathing room as debt payments vanish

- Income Efficiency: Keep more of your money, month after month after month

- Growing Equity: Watch equity swell as mortgage balance dwindles

- Obliterate Interest: Early mortgage payoff, release a flood of cash to grow true wealth

What's Within Your Grasp?

Picture this: effortlessly writing that check for your kid's next semester of college. No more sweating the big-ticket items. Drive off the lot in a new car without chaining yourself to a 5-year, $5-900-a-month car note. Jet off for a month of adventure just because you can. Cover your daughter's dream wedding without resorting to organ trafficking. Own a whopping 70-90% of every dollar you earn. Shrug off nearly all your financial worries. Lock in your rock-solid retirement in your 40s or 50s. That's what's waiting for you, my friend.

OVERCOMING THE CHALLENGE:

EXECUTING THIS SOLO, ESPECIALLY IF YOU'VE FOLLOWED THE HERD FOREVER, CAN BE DAUNTING.

SOLO PILGRIMAGES ARE FOR THE BRAVE - NOT THE WISE.

But rejoice, you’re not alone in this endeavor: You’ll be a part of a community of like-minded people, who know that The Shred Method™ tool guides every dollar, ensuring it works its magic optimally.

Precision is key; the software orchestrates payments and extras based on intricate algorithms. It's like a symphony for your finances, reducing interest noise to a whisper.

Simply plug your data into the software. Balances, rates, payments – it calculates your debt's demise timeline. Savings stack, wealth burgeons. The difference between Shred and the mainstream route? Often seven to eight figures.

The Critical Juncture

Ready to break free? Two steps await:

-

Register for The Shred Method™ comprehensive course, software and community

-

If you’re still on the fence, book a complimentary discovery call

The decision is yours:

ARE YOU GENUINELY COMMITTED TO PUMMELING DEBT?

If yes, your path to freedom starts with a single click below.